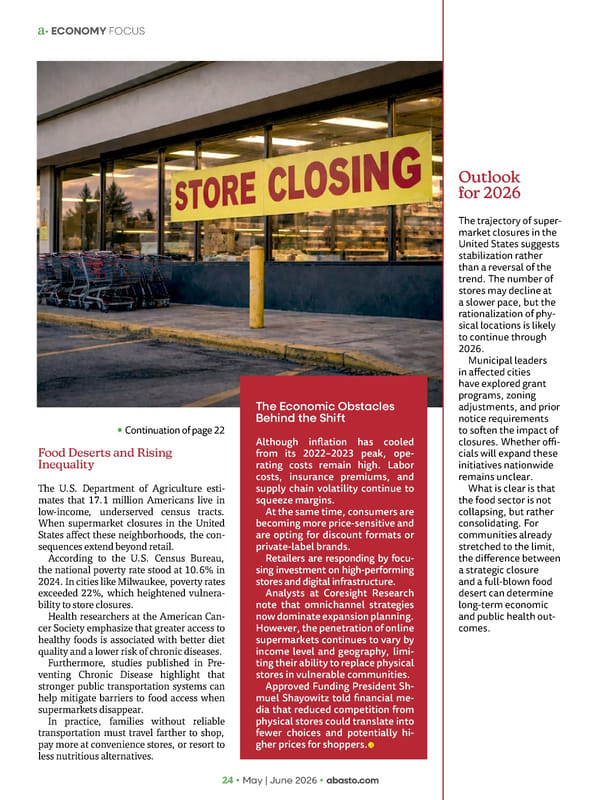

24 • May | June 2026 • abasto.com The Economic Obstacles Behind the Shift Although inflation has cooled from its 2022–2023 peak, ope- rating costs remain high. Labor costs, insurance premiums, and supply chain volatility continue to squeeze margins. At the same time, consumers are becoming more price-sensitive and are opting for discount formats or private-label brands. Retailers are responding by focu- sing investment on high-performing stores and digital infrastructure. Analysts at Coresight Research note that omnichannel strategies now dominate expansion planning. However, the penetration of online supermarkets continues to vary by income level and geography, limi- ting their ability to replace physical stores in vulnerable communities. Approved Funding President Sh- muel Shayowitz told financial me- dia that reduced competition from physical stores could translate into fewer choices and potentially hi- gher prices for shoppers. • Continuation of page 22 Food Deserts and Rising Inequality The U.S. Department of Agriculture esti- mates that 17.1 million Americans live in low-income, underserved census tracts. When supermarket closures in the United States affect these neighborhoods, the con- sequences extend beyond retail. According to the U.S. Census Bureau, the national poverty rate stood at 10.6% in 2024. In cities like Milwaukee, poverty rates exceeded 22%, which heightened vulnera- bility to store closures. Health researchers at the American Can- cer Society emphasize that greater access to healthy foods is associated with better diet quality and a lower risk of chronic diseases. Furthermore, studies published in Pre- venting Chronic Disease highlight that stronger public transportation systems can help mitigate barriers to food access when supermarkets disappear. In practice, families without reliable transportation must travel farther to shop, pay more at convenience stores, or resort to less nutritious alternatives. • ECONOMY FOCUS Outlook for 2026 The trajectory of super- market closures in the United States suggests stabilization rather than a reversal of the trend. The number of stores may decline at a slower pace, but the rationalization of phy- sical locations is likely to continue through 2026. Municipal leaders in affected cities have explored grant programs, zoning adjustments, and prior notice requirements to soften the impact of closures. Whether offi- cials will expand these initiatives nationwide remains unclear. What is clear is that the food sector is not collapsing, but rather consolidating. For communities already stretched to the limit, the difference between a strategic closure and a full-blown food desert can determine long-term economic and public health out- comes.

Abasto Magazine - May/June 2026 ENGLISH Page 23 Page 25

Abasto Magazine - May/June 2026 ENGLISH Page 23 Page 25